Audit Procedures for Cash and Cash Equivalents

Key Audit Procedures for Cash and Bank Audit The first important task for the auditor is to get a clear understanding of the clients policy and procedure for cash. Item 1 - Cash Item 2 - Cash Item 3 - Cash Item 4 - Other Assets Item 5 - Investment Item 6 - Investment current Item 7 - Cash Item 8 - Cash Item 9 - Current liability Item 10 Offset to cash Item 11 Offset to Cash Item 12 Unused supplies Item 13 Cash as cash equivalents Item 14 Short-term investment Item 15 Cash Item 16 Cash Item 17 property recorded as.

Audit Of Cash And Bank Balances

Provide cash and cash equivalents faster than usual.

. C establish the completeness of recorded cash. 2 Full PDFs related to this paper. The term audit would mean that you need to apply auditing procedures on cash and bank accounts of the company.

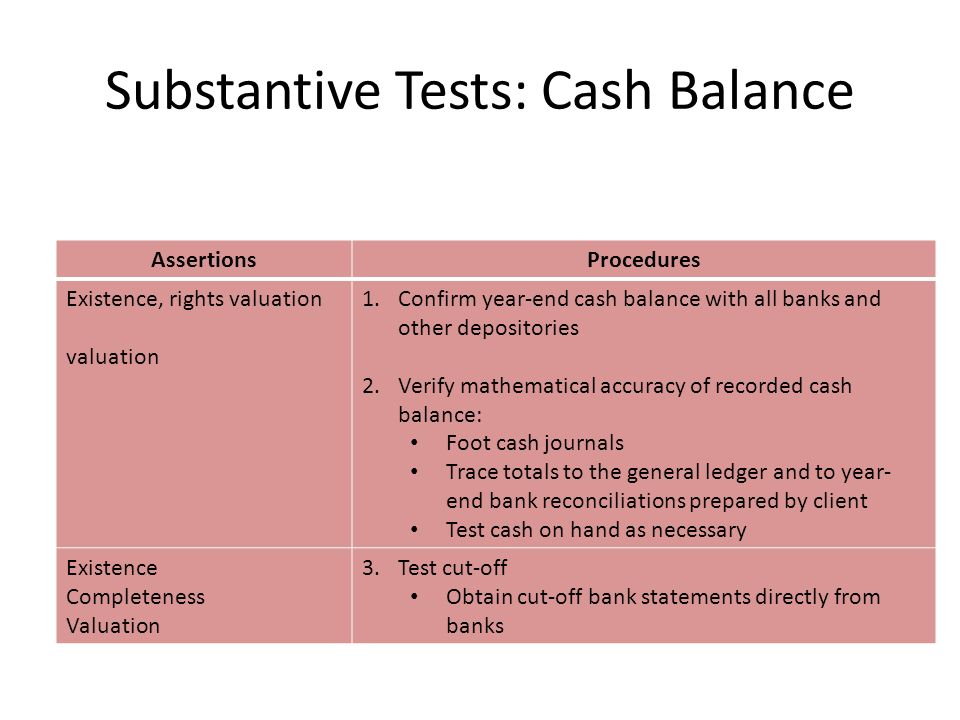

All of the entitys cash is included - Perform cash cutoff test. D verify the cutoff of cash transactions. Recorded balances are complete and stated at realizable amounts.

This site is like the Google for academics science and research. The cash must exist under company control at the reporting in. Cash recorded on the books exist-Count cash on hand-Confirm bank balances-Examine interbank transfers.

Based on the application of the necessary audit procedures and appreciation of the above data you are to provide the. Substantive Analytical Procedure for Cash. 6 rows Audit Procedures for testing Cash and Cash Equivalents include Test of Controls and.

Identify the risk of fraud related to cash and cash equivalents. Audit procedures for cash. Test of Detail for.

AUDIT PROCEDURES FOR CASH CASH EQUIVALENTS MODULE CONTENTSOBJECTIVES. AUDITING CASH CASH EQUIVALENTS. Check and agree the.

Account for all cash. 4 rows Following procedures are usually used for bank reconciliation in audit cash. Collection by bank of companys notes receivable 71815 80900 The bank statements and the companys cash records show these totals.

Based on the above and the result of your audit how much will be reported as cash and cash equivalent at December 31 2006. In this role as an external auditor of company ABC ie as a member of the external audit team you have to audit bank balances of the company as well as cash in hand. Textbook Solutions Expert Tutors Earn.

Prepare accurate cash budgets. - Perform analytic procedures. Audit Assertion for Cash and Cash Equivalent.

Cash and cash equivalents control procedures. Recorded balances exist and are owned by the institution. The principal objectives of the substantive procedures for cash are to.

The following are the substantive audit procedures for cash. Identifying audit risks in cash and bank balances. Obtain the bank reconciliation statements for all the bank accounts and test the reconciling items.

A substantiate the existence of recorded cash and the occurrence of cash transactions. Retain documentation for all items of expenditure. Balances are properly presented in the financial statements.

The auditor will need to compare cash balances to the prior period in order to examine if there is. 1 Audit Objective The objective of this template is to ensure the Completeness Accuracy Existence and Valuation of cash and cash equivalents. Adhere to general principles for cash control.

This video lecture discusses the audit of cash and cash equivalents particularly the substantive procedures to be performed on the said line item. Savings account at PS Bank P1200 Checking account at PS Bank 1800 Petty cash fund 10 Currency and coin 15 Total P3025 Answer. Describe designing a detailed audit plan linking assessed risk to planned procedures.

AUDIT OF CASH AND CASH EQUIVALENTS SUBSTANTIVE AUDIT PROCEDURES FOR CASH Cash Balances Existence. 625 The primary audit objectives for cash are to obtain reasonable assurance that. Full PDF Package Download Full PDF Package.

Articles News Stories Published. A short summary of this paper. Obtaining evidence related to cash and cash equivalents.

Disbursements in July per bank statement P218373 Cash receipts in July per Mathildas books 236452 Questions. B determine the valuationaccuracy of cash transactions. Cash and cash equivalent are the most liquidated assets on the financial.

- Prepare proof of. Share Cash and Cash Equivalents Audit Procedures CONDINO. Implement physical cash limits.

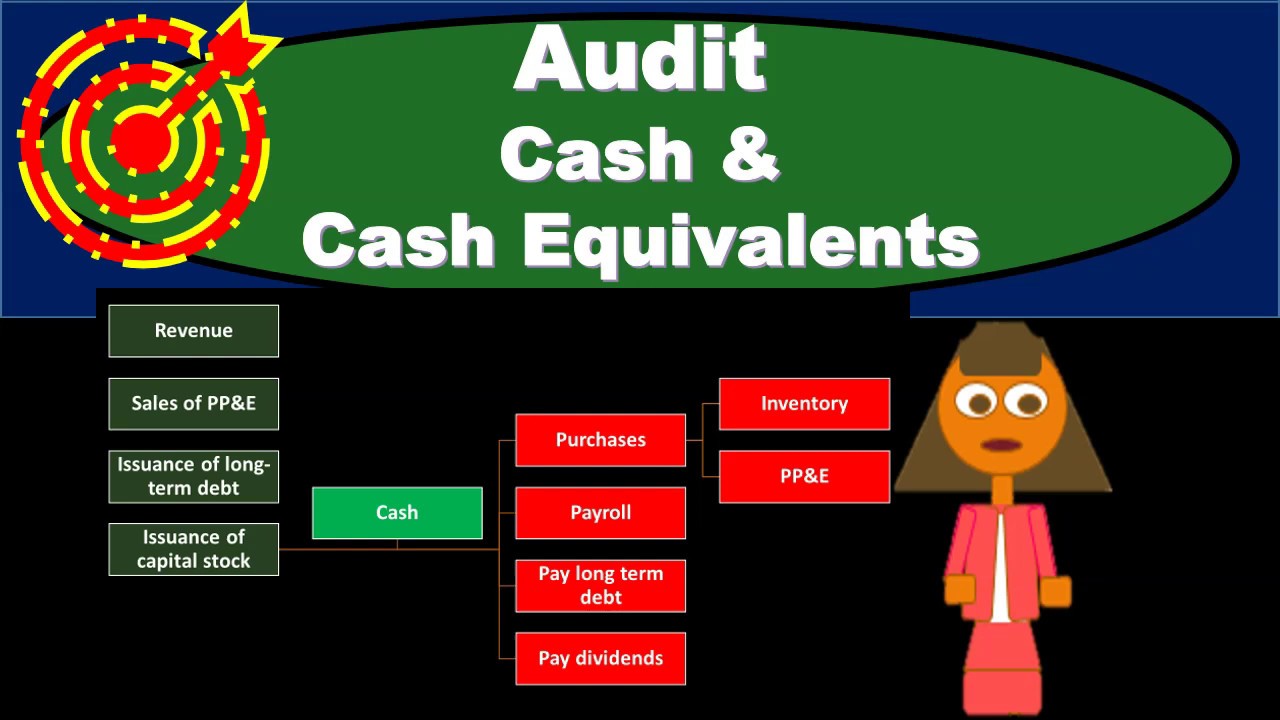

Techniques used to perform the audit procedures associated with auditing cash and cash equivalents. How to Audit Cash and Cash Equivalent. 2 Summarized Business Cycle Cash and Cash equivalent Description.

CPA Engagement Lead-Risk Identified-procedures-Cash Cash-equivalent June 2015 Description.

Audit Cash And Cash Equivalents Pdf Cheque Deposit Account

Liquid Assets Accounting And Finance Learn Accounting Accounting Education

Audit Cash Cash Equivalents Youtube

Cash Audit Procedures Assertions Objectives Management Cash Exists Include All Transactions That Should Be Presented Represents Rights Of The Entity Ppt Download

0 Response to "Audit Procedures for Cash and Cash Equivalents"

Post a Comment